Obtenir le modèle :

Résumer cet article avec :

At the start of every new business relationship, many questions arise.

Is this new customer reliable? Should you grant them a payment term or request a deposit?

If so, for how long? What should the credit limit be?

All these questions are legitimate and key to analysing customers properly and protecting your business from bad payers.

To help answer them, the credit score is a valuable indicator to analyse.

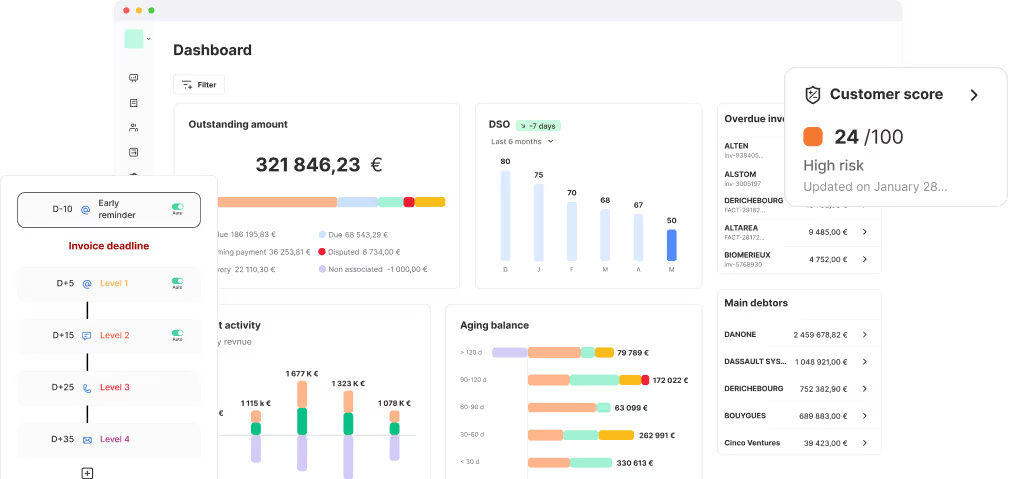

In LeanPay, you can also manage customer risk. The platform is integrated with several partners (CreditSafe, Altares, Allianz Trade, Coface, and more) that provide credit scoring and maximum outstanding amounts not to be exceeded. Within LeanPay, you’re automatically alerted in case of insolvency proceedings or when a customer’s outstanding balance goes over the authorised limit.

Credit scoring: definition

Credit scoring assigns a score to a prospect or customer.

This score reflects their financial strength based on several financial, legal and behavioural criteria.

Past experiences, meaning all the underlying criteria, are converted into data to help predict future behaviour.

Credit scoring provides a probability that a prospect or customer will meet their financial commitments.

In simple terms:

- Company A, showing signs of financial distress, will have a lower credit score and therefore a higher risk of default.

- Company B, showing positive indicators, will have a stronger credit score and therefore a low risk level.

This scoring method is used in credit risk management. It helps assess, through a simple metric, the financial risk related to a company.

The advantage: decisions are based on objective data, not subjective feelings or past experiences.

Credit score is a key decision-making tool for finance teams. But not only!

Sales teams also value it, since they know the finance department may refuse risky orders or impose stricter payment terms that are hard to negotiate.

Having access to such data allows sales teams to avoid high-risk prospects and save time in their pipeline management.

I find this debt collection software very functional, with excellent tracking of reminders and a clear, precise dashboard. Customer service is responsive.

Stéphanie H. - Collections Officer

Discover LeanPay 👉

Credit scoring: how to calculate it

The pre-sales score and the behavioural score

There are two main types of scores in credit scoring:

- Pre-sales score

This one is calculated before entering a commercial relationship.

It determines whether the prospect can become a customer and under what conditions.

If the score is poor, the company will never be a customer.

If it’s positive, the score is refined to define contractual conditions, payment terms, and credit limits.

- Behavioural score, once the company becomes a customer

This second score is based on the customer’s payment behaviour and serves to predict future behaviour.

It can be combined with the pre-sales score to determine the final credit score.

The criteria of credit scoring

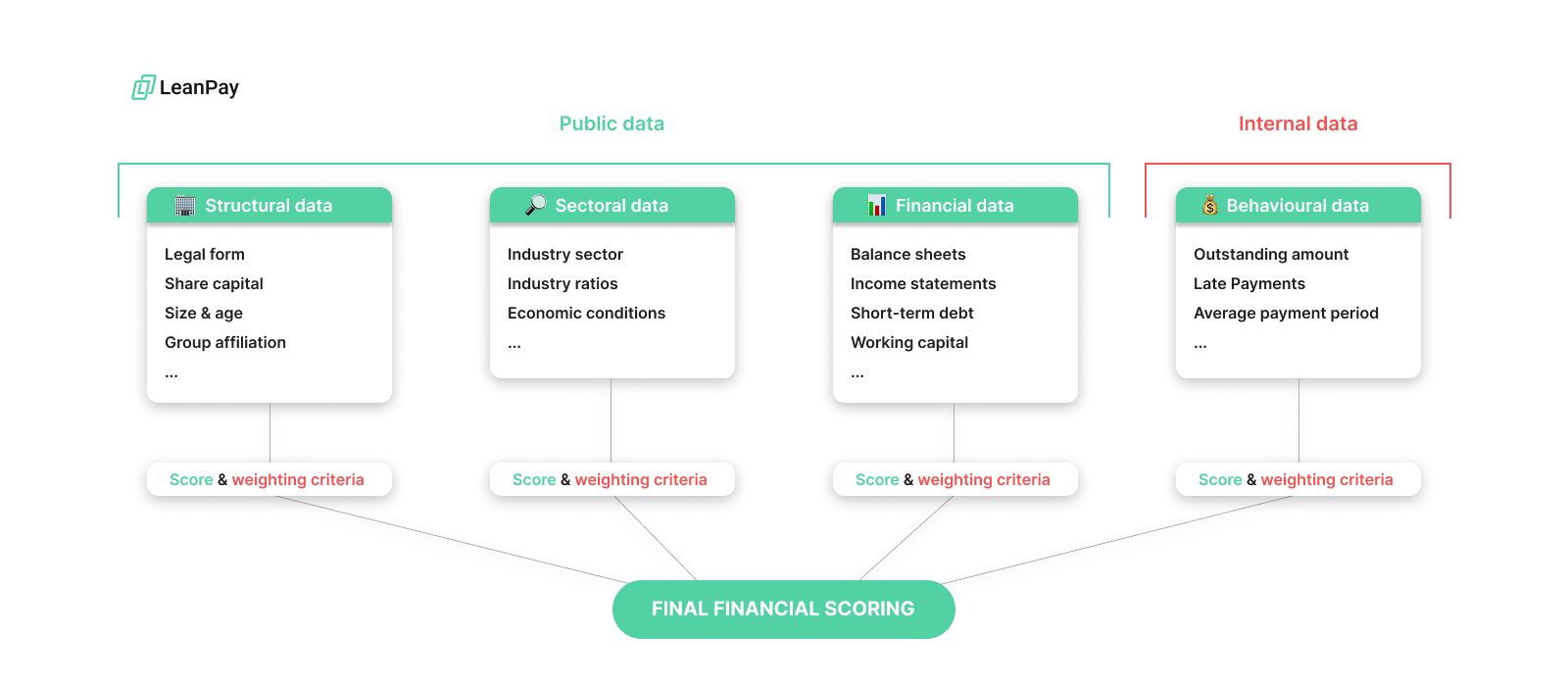

Several indicators are used in calculating a company’s credit score:

- Structural data:

Legal form, share capital, age, size, geographical location, executives, group ownership (which may imply financial security through a parent company), company history etc.

- Sector data:

Industry sector, sector ratios, economic conditions, and resilience capacity (e.g. COVID-19 crisis, energy crisis…).

- Financial data:

Solvency ratios, balance sheets, income statements, short-term debts, working capital, operating capital… All used to assess solvency and financial performance.

- Behavioural data (your own customer data):

Outstanding amount, late payments, average payment delay, ongoing disputes.

The aim is to identify the customer’s ability to pay on time.

Many of these elements are available freely online.

Together, these four categories produce the final credit score of the customer.

It’s also recommended to weight certain criteria according to their importance when calculating the final score.

This weighting can be adjusted depending on customer type, sector, or company size (SME, mid-market, large account).

Weighting helps reduce bias. A “bad” score doesn’t necessarily mean the customer is in trouble.

Likewise, a good score doesn’t always guarantee safety. The key is to compare the score against the sector average.

For instance, a company with a modest score but still above its sector average may actually be a promising prospect.

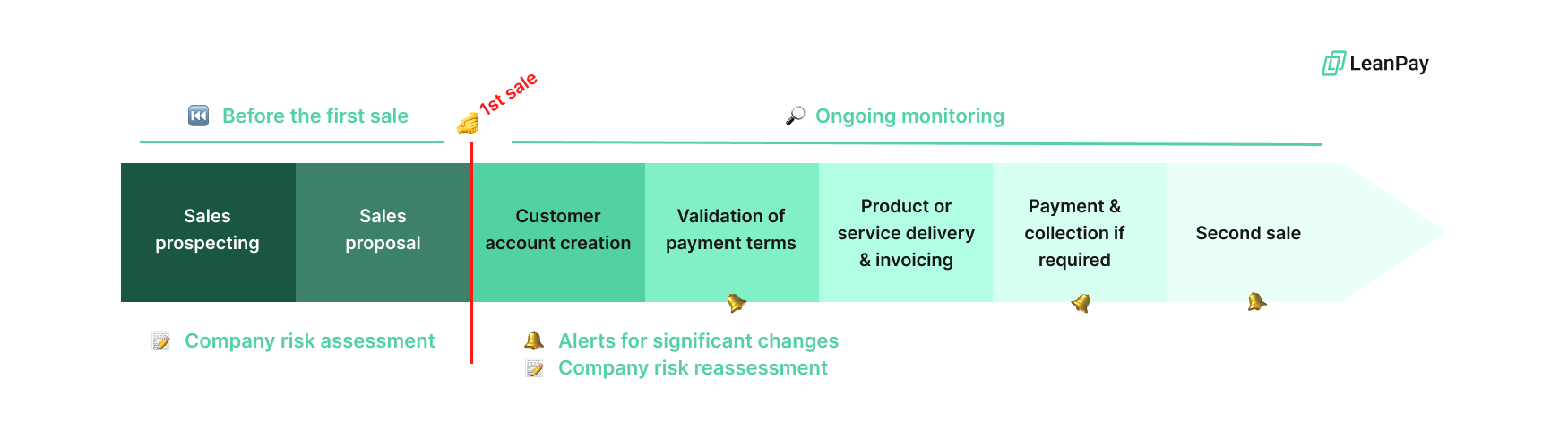

When should you measure credit scoring?

At what stage should credit scoring be performed and how often?

In risk management, it’s recommended to assess credit scoring both before a commercial relationship begins and regularly afterwards, especially when key changes could affect the score.

Before the sale (pre-sales phase)

Naturally, credit scoring should be done before the prospect becomes a customer, during the prospection or proposal phase.

It’s a way to choose customers wisely. In Europe, 25 % of bankruptcies are caused by unpaid customer invoices. Companies don’t collapse because of lack of business, but because their customers pay too late or not at all.

That’s why it’s essential to assess financial health early on.

During this pre-sales stage, all relevant company data should be gathered and verified for the credit score.

If the number of prospects makes this task too time-consuming, you can rely on specialised credit rating firms to assist you, or set a minimum outstanding amount from which this verification becomes mandatory.

Ongoing monitoring (post-sale phase)

Once a prospect becomes a customer, credit scoring must be monitored regularly.

The goal is continuous vigilance throughout the business relationship.

“Regularly” means assessing the score whenever a significant change could affect risk level.

You can even set up real-time alerts for any relevant update.

Key signals to watch:

- Company status (active or dissolved)

- Change in payment behaviour

- Publication of a new financial statement

- Change in management

- Economic downturn or market shift

- …

How to interpret the credit score

The final credit score, for example on a scale of 0 to 100, can be linked to a risk level such as:

Each company can define its own risk equivalence.

This makes it easier to focus on high-risk customers, those with large outstanding amounts or strategic importance.

Over time, repeated evaluations create a credit score history.

Analysing its evolution is highly insightful: if the score has been declining for months, it’s a serious red flag.

All these indicators help guide decisions for each risk level.

For example:

- On a micro scale: do not grant credit to high-risk customers, or impose stricter payment limits.

- On a macro scale: if most customers show strong scores and low risk, focus analysis only on high-risk cases. But if many customers have weak scores and high risk, it’s time to rethink your sales policy.

Obtenir le modèle :

Obtenir le modèle :