Obtenir le modèle :

Résumer cet article avec :

Late payments quickly put pressure on cash flow and absorb a significant amount of time for finance teams. In this context, the promise to pay becomes a key tool to structure collections and regain short term visibility.

When properly worded and carefully followed up, a promise to pay helps unblock situations that have stalled, sets a usable payment date and improves short term cash visibility. Still, it must be requested at the right time, formalised correctly and monitored closely, especially if it is not honoured.

This article explains how a promise to pay becomes a real collections lever and how LeanPay makes it easy to track on a daily basis.

Promise to pay: an underestimated lever to unlock overdue invoices

A promise to pay is a debtor’s commitment to settle an outstanding invoice on a specific date. It goes far beyond a simple verbal agreement and becomes a concrete reference for collections follow up. When clearly formulated, it represents a moral commitment that clarifies the situation, sets a specific date and restores visibility for teams in charge of collections.

I find this debt collection software very functional, with excellent tracking of reminders and a clear, precise dashboard. Customer service is responsive.

Stéphanie H. - Collections Officer

Discover LeanPay 👉When should you use a promise to pay in collections?

A promise to pay can be used at several stages of the reminder process:

- When the debtor acknowledges the debt but cannot pay immediately

- In this situation, the promise to pay turns a temporary difficulty into a realistic deadline while keeping the relationship active.

- When reminders reach a deadlock

- Asking for a promise provides an alternative to repeated reminders. It encourages the debtor to propose a specific date and reintroduces a dynamic of commitment.

- After a dispute has been resolved

- Once the dispute blocking payment has been cleared, the promise to pay confirms the return to a normal payment cycle and secures a payment date so the invoice can be reintegrated into follow up.

In all these cases, the goal is to formalise a short term agreement to put the invoice back on a payment trajectory.

Promise to pay: signals that indicate it can be effective

Certain factors increase the likelihood that a promise to pay will be respected:

- A responsive debtor

- Responsiveness shows that the issue is taken seriously and that the invoice has not been sidelined. This is often a good indicator of short term solvency.

- Clear and structured communication

- The more precise the exchanges, the easier it is to agree on a realistic date. It also shows that the debtor understands their situation and payment capacity.

- Explicit acknowledgement of the debt

- When the debtor confirms the outstanding amount, the promise fits into a coherent framework. The obstacle is temporary rather than structural.

Conversely, vague commitments or a lack of responsiveness should raise concerns about non payment risk.

How to use a promise to pay to accelerate cash collection

Obtaining a promise to pay is not enough on its own. It must be used properly to structure the next steps in collections and genuinely increase the chances of payment. When leveraged effectively, it becomes a clear reference point that helps adapt the collections strategy and improve short term visibility.

Formalising the commitment to secure the exchange

To be effective, a promise to pay must be clearly defined and recorded. Not all promises have the same value:

- A verbal promise can be sufficient during a phone call, but it is difficult to use internally.

- A written promise by email or via a customer portal is more reliable, as it clearly states the date and amount.

- A structured promise including amount, date, payment method and invoice reference is the most robust, as it can be fully integrated into collections follow up.

Including the essential elements

In all cases, certain information should always be included:

- The amount concerned, to avoid any ambiguity, especially when several invoices are involved.

- The exact payment date, as a promise without a defined date is of little value for collections management.

- The planned payment method, such as card, bank transfer or direct debit, since bank processing times vary.

- The invoice or case reference, which is necessary to correctly link the promise to the relevant invoice and track its status.

Formalising these elements turns a simple exchange into a concrete operational commitment that can be used by both the collections team and finance management.

Integrating the promise to pay into ongoing follow up

A promise to pay only has an impact if it becomes the new reference point for follow up. As soon as a debtor commits to a date, that date replaces the original due date when organising the next collections actions.

The reminder strategy must therefore adapt to avoid sending unnecessary messages when an agreement has just been reached. This helps prevent inappropriate reminders that could damage the customer relationship. At the same time, the invoice should remain visible in overdue monitoring, even if reminders are temporarily paused. The aim is to stay alert without applying unnecessary pressure.

How a promise to pay improves cash forecasting and short term visibility

A promise to pay is not only useful for organising collections. It also provides valuable information for anticipating incoming payments and assessing debtor behaviour. When interpreted correctly, it becomes a reliable indicator of short term cash visibility and customer risk.

Why is a promise to pay better than a simple intention?

A structured promise, with a defined date and amount, offers far more visibility than a vague statement such as “we will pay soon”.

It makes it possible to:

- Integrate a realistic collection assumption into short term cash forecasts.

- Distinguish invoices in the process of being settled from those genuinely at risk.

- Adjust cash decisions such as supplier payments or short term priorities.

A promise to pay does not guarantee payment, but it provides a concrete reference point that reduces uncertainty and improves follow up.

Is a promise to pay actually reliable?

The reliability of a promise to pay depends as much on context as on debtor behaviour. Several common patterns can be observed:

- Punctual debtors who announce realistic dates and usually meet them.

- Debtors who systematically postpone the announced date.

- Debtors with limited visibility who make repeated promises without being able to honour them.

Rather than calculating an average fulfilment rate, it is more relevant to analyse the dynamics within your own portfolio. Which customers keep their commitments? Which profiles are more inconsistent? Which delays are due to one off issues versus structural cash constraints?

This contextual analysis makes it possible to adjust the level of trust granted to each promise and to adapt both reminder strategies and cash forecasts.

When a promise to pay becomes a risk signal

Certain situations should raise alerts, as they indicate that the promise to pay reflects fragility rather than good faith:

- A commitment given without any concrete justification.

- A promise not honoured even though it seemed realistic.

- Dates repeatedly postponed without clear explanation.

- Inconsistent or contradictory statements across exchanges.

When these signals appear, the promise should be treated with caution. It may justify stronger reminders, a request for additional guarantees or escalation to a more formal collections stage.

How to track promises to pay efficiently with LeanPay

Our debt collections software allows promises to pay to be recorded and tracked directly from invoices, while automatically adjusting reminders and outstanding amounts. The objective is to secure debtor commitments without additional manual processing.

A clear status that automatically adjusts follow up

When a promise to pay is recorded, the relevant invoice is temporarily excluded from reminders while remaining visible in the outstanding amount.

.png)

If the promise to pay is not honoured on the agreed date, the invoice automatically re enters the reminder plan and becomes overdue again based on its status.

A notification immediately flags the broken promise so action can be taken quickly.

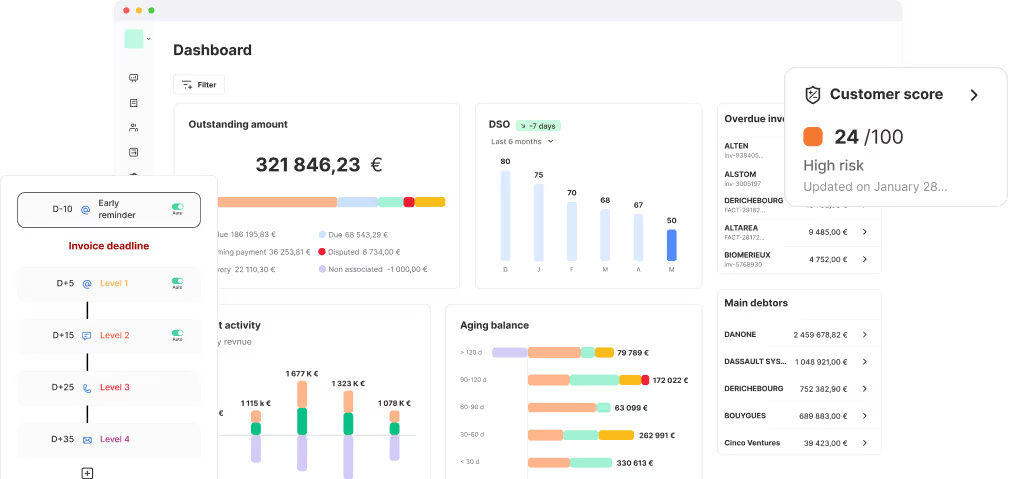

Consolidated visibility within the outstanding amount

In the accounts receivable dashboard, promises to pay can be identified in:

- The overall outstanding breakdown.

- A dedicated “Promise to pay” category within outstanding amount analysis.

- Invoice status lists.

.png)

This makes it easier to isolate committed amounts, anticipate expected cash inflows and identify promises approaching their due date.

A complete history to understand debtor behaviour

LeanPay keeps a full history of all promises associated with an invoice, accessible from the customer record or directly from the invoice. Team comments provide full visibility on:

- Announced dates.

- Any postponements.

- Promises honoured or missed.

This history supports payment behaviour analysis and strengthens risk prevention at portfolio level.

LeanPay includes many features that help more than 3 000 finance teams reduce their DSO by at least 40 percent. Discover them during a demonstration with one of our experts.

Promise to pay: FAQ

What is a promise to pay?

A promise to pay is a commitment made by a debtor to settle an invoice on a specified date.

Does a promise to pay have legal value?

No. It is based on a moral commitment from the debtor and mainly serves as a reference point to organise reminders and anticipate cash inflows.

How do you record and track a promise to pay?

A promise to pay should be recorded with the amount, payment date and invoice reference, then tracked until settlement. Dedicated collections software helps automate follow up and reduce manual work.

What should you do if a promise to pay is not honoured?

A broken promise should be treated as a risk signal. It justifies:

- Resuming reminders immediately.

- Requesting a new date with clear explanations.

- Adapting the collections strategy if postponements become recurrent.

Obtenir le modèle :

Obtenir le modèle :