Obtenir le modèle :

Résumer cet article avec :

When a customer starts facing financial difficulties, the impact rarely stops at a simple delay in payment. It can trigger a chain reaction that weakens their entire activity and, in turn, yours. In a context where business failures remain at record levels and payment delays are increasing, anticipating default risk has become a strategic priority for protecting your cash flow.

The key question is no longer just whether a customer will pay, but when the first warning signs should alert you. In this article, you will learn how to analyse risk, identify the most exposed customers and structure your organisation to reduce the impact of a major unpaid invoice.

Default risk: why the domino effect directly impacts creditors

Default risk should never be underestimated. When a customer goes bankrupt, it affects their entire ecosystem: suppliers, service providers and, ultimately, all those still waiting for payment.

In developed countries, business failures increased by 20% in 2024 and a further 5% in 2025, according to Coface. In 2026, an additional increase of nearly 3% is expected.

In an already fragile environment, even a minor disruption can trigger a much faster chain reaction than before.

This vulnerability is further reinforced by certain practices among large companies. Extended payment terms imposed by major buyers shift financial pressure onto SMEs. Their cash flow deteriorates, their insolvency risk increases, and this can ultimately trigger a cascade of defaults across their network.

I find this debt collection software very functional, with excellent tracking of reminders and a clear, precise dashboard. Customer service is responsive.

Stéphanie H. - Collections Officer

Discover LeanPay 👉

Default risk: how to identify your most exposed customers

Identifying the most vulnerable customers is the first step in managing default risk effectively. Not all accounts carry the same weight or level of exposure. Some customers represent a significant share of your outstanding amount, while others show early warning signs of financial deterioration.

Default risk: identify customers with high exposure

A customer becomes critical not only because they pay late, but also because they represent a large share of your revenue. High concentration increases the impact of any payment incident.

To assess this level of exposure, consider:

- the share of revenue generated by the customer

- the outstanding amount already committed

- actual payment behaviour

- the sensitivity of the sector they operate in

The more these factors point towards vulnerability, the greater the potential impact on your cash flow.

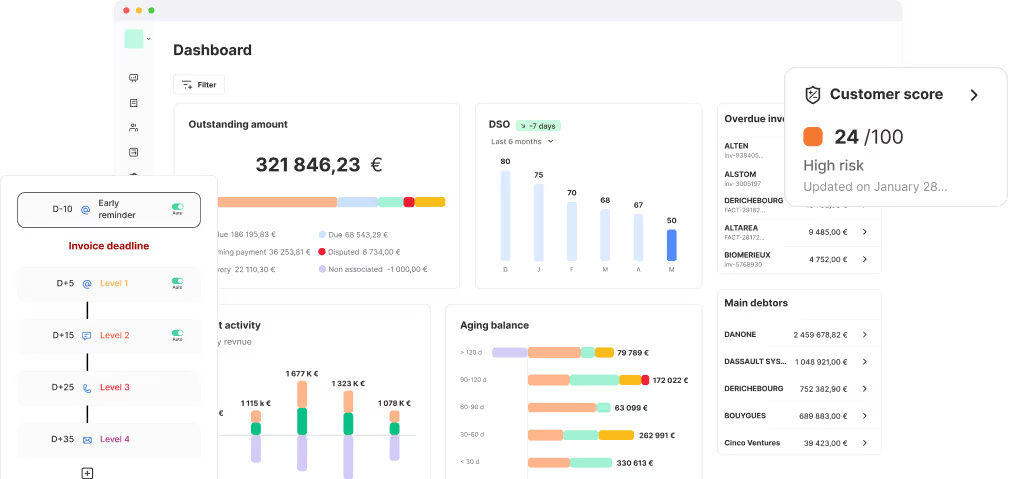

With our credit risk management software, this prioritisation becomes much easier. Key indicators are centralised for each customer, allowing you to quickly identify high-risk accounts and prioritise actions.

.png)

Default risk: detect early warning signs in payment behaviour

Even before a payment default occurs, certain behaviours indicate that a customer’s situation is deteriorating. These early signals are often the first signs of default risk. Spotting them early allows you to adapt your reminder strategy immediately.

Common warning signs include:

- recurring or increasing payment delays

- unusual requests for extended payment terms

- broken payment promises

- prolonged lack of response despite multiple reminders

- growing or unexplained disputes

When these signals accumulate, they often indicate that a customer is struggling with cash flow or prioritising payments.

LeanPay helps you monitor these signals effectively. Disputes can be recorded, categorised and tracked, payment promises are logged, and average delay is visible directly in the customer profile. This visibility allows you to detect risk earlier.

Default risk: monitor operational warning signs

Some warning signs are not financial or legal, but operational. They often reveal early signs of organisational stress within your customer’s business.

These may include:

- a drop in order volumes or irregular purchasing patterns

- longer delays in obtaining approvals or required documents (proof of service, confirmations, etc.)

- frequent changes in contacts or visible internal disorganisation

Taken together, these signals often indicate operational fragility. While not proof in themselves, changes in rhythm or organisation should raise concerns, especially when combined with payment delays.

Default risk: external signals you should monitor

Payment behaviour alone is not enough to fully assess default risk. To get a complete picture, you also need to consider external signals. They often provide a more structural view of a customer’s financial health and allow you to anticipate issues earlier.

Default risk: sector risks and dependencies

Some risks stem not from the customer itself, but from the sector they operate in.

Public signals may include:

- sectors identified as high-risk in market reports (Dun & Bradstreet, Coface, etc.)

- rising failure rates within a specific industry

- major company closures, restructurings or regulatory pressure widely reported in the media

These signals should prompt closer monitoring, as sector-wide shocks quickly impact company cash flow.

Default risk: public financial and legal indicators

Beyond payment behaviour and sector context, certain publicly available financial and legal indicators can signal insolvency risk. They provide an external, yet useful, view of a company’s situation.

- solvency alerts from financial data providers

- entries in official registers

- significant changes in company data (management changes, capital reductions, etc.)

When combined with unusual payment behaviour or a sector already under pressure, these signals should prompt increased vigilance.

Thanks to integrations with leading financial data providers and credit insurers, LeanPay gives you access to real-time credit scoring and recommended credit limits, helping you anticipate risk. You are also alerted when a customer enters insolvency proceedings.

Default risk: how to anticipate and limit the domino effect

The domino effect occurs when the weakness of one customer leads to delays, then unpaid invoices, and ultimately puts pressure on your own cash flow.

Reducing this risk requires more than monitoring signals. You need to structure your accounts receivable management to prioritise, adapt and anticipate.

Default risk: organise your accounts receivable by risk level

To avoid being impacted by customer defaults, you must structure your portfolio based on risk levels. This makes it possible both to identify which accounts should be treated as a priority and to maintain an overall view of how the portfolio is evolving over time.

This involves:

- classifying customers by risk level based on observed signals

- adapting monitoring frequency (daily for high-risk accounts, regular for others)

- continuously updating classifications based on delays, disputes, payment promises and sector context

- sharing risk visibility across finance, sales and management teams

In LeanPay, this prioritisation is simplified through reporting filters. Applying the “Risk” filter automatically isolates high-risk segments of your portfolio (outstanding amount, overdue invoices, DSO). These indicators are updated in real time, allowing you to focus on urgent actions.

.png)

In addition, you can schedule the automatic sending of a dashboard report, so that you can receive and/or share key accounts receivable indicators at regular intervals, either weekly or monthly.

Default risk: adapt your reminder strategy

As default risk increases, your reminder strategy must adapt quickly and become more structured. In particular, you can:

- shorten intervals between reminders

- increase formalisation (letters, stronger tone, more structured communication)

- systematically document exchanges (dates, commitments, supporting documents)

- anticipate pre-legal actions when warning signs escalate (broken payment promises, unresolved disputes, no response)

With our debt collection software LeanPay, you can create customised reminder workflows based on your criteria. If a customer’s behaviour changes, a more appropriate workflow can be automatically assigned. You simply need to create an automation rule by selecting the condition and the resulting action.

For example:

if DSO exceeds 60 days → assign “high-risk customer” workflow

.png)

More than 3 000 finance teams have reduced their unpaid invoice risk to below 1% with LeanPay.

Get in touch to achieve the same results.

Obtenir le modèle :

Obtenir le modèle :