Obtenir le modèle :

Résumer cet article avec :

In many mid-sized businesses, collections still rely on generic rules applied uniformly across all customers:

- the same timescales,

- the same messages,

- the same workflows.

Regardless of payment profile or behaviour.

The result is reminders that go out too late, misdirected effort and a DSO that keeps creeping up.

Predictive analytics offers a different approach. It helps finance teams anticipate late payments and focus their efforts where they will have the most impact.

In this article, we look at the principles behind predictive analytics and how it applies to collections in practice, to understand how this technology is changing the way businesses manage their accounts receivable.

Predictive analytics: definition

Predictive analytics means using past and present data to anticipate future events. It relies on predictive models, statistical tools that process this data to estimate the likelihood of a given event occurring.

The goal is not to "predict the future", but to support better decision-making based on measurable signals.

In a financial context, this might mean anticipating the risk of a late payment, a default, or a cash flow strain.

In practice, predictive analytics is often part of a broader data analysis approach:

- Descriptive analytics explains what has already happened (for example, the late payment rate over the past six months).

- Predictive analytics anticipates what could happen next (which invoices are at risk of being paid late).

- Prescriptive analytics recommends what action to take (chase a specific customer on a specific date via a specific channel).

I find this debt collection software very functional, with excellent tracking of reminders and a clear, precise dashboard. Customer service is responsive.

Stéphanie H. - Collections Officer

Discover LeanPay 👉

How predictive analytics works in finance and collections

In predictive analytics finance, the primary goal is to anticipate payment behaviour and assess the likelihood of delays or defaults. The process typically follows three steps.

Collecting and making use of the right data for predictive analytics

Everything starts with bringing together the right data, drawn from both internal tools (ERP, CRM, invoicing or debt collection software) and external sources such as financial information providers. This information builds a complete picture of each customer's payment behaviour:

- payment history per customer: average payment times, delays, amounts, frequency

- customer data: sector, size, length of the commercial relationship

- contextual indicators: economic conditions, seasonality, financial situation

Together, this data makes it possible to build a payment profile for each customer.

The more complete and reliable the data, the more accurate the predictions.

Training the predictive model

This data is then processed by a predictive model, trained to recognise payment patterns and estimate key indicators such as:

- the probability of a late payment or unpaid invoice

- the average expected payment time

- the overall risk score for a given customer

The model uses statistical techniques and machine learning to identify recurring behaviours: systematic delays above certain amounts, sector-specific variations, or early warning signals of cash flow pressure.

Thanks to machine learning, it continuously improves its accuracy as it processes new data

Interpreting and acting on predictive analytics

The value of predictive analytics lies not just in producing numbers, but in guiding the decisions that follow:

- prioritising payment reminders based on risk level

- adjusting the tone, channel or frequency of communications

- triggering proactive alerts before an invoice falls due

- routing the most sensitive cases to a human review or legal recovery process

Used day to day, it becomes a decision-support tool for credit management: it does not replace human expertise, but reinforces it by providing objective, prioritised signals.

Predictive analytics: the benefits for finance teams

Predictive analytics is reshaping the finance function. CFOs and credit managers are no longer limited to reacting to late payments after the fact; they can anticipate them and factor them into the operational management of customer risk and cash flow.

A forward-looking view of customer risk

Predictive analytics provides a detailed map of the customer portfolio: risk levels, probability of delay, and how payment behaviour is evolving over time.

This visibility helps finance teams anticipate cash flow pressure, adjust commercial terms (payment deadlines, guarantees, credit limits) and concentrate efforts on the highest-risk segments.

More reliable cash flow management with predictive analytics finance

By incorporating payment probabilities into cash flow forecasts, finance teams get a more realistic picture of future receipts.

They can adjust their financing needs, prevent overdrafts and optimise their working capital requirements, thanks to more granular short and medium-term projections.

This approach improves the reliability of financial planning and the precision of cash flow decisions.

Faster, better-informed decisions

Predictive scoring makes it easier to take well-grounded decisions, such as whether to grant an extension or trigger a pre-due date reminder.

Every decision is based on hard data rather than gut feeling, which improves responsiveness and alignment across finance, collections and commercial teams.

A platform for sustained performance

Beyond the immediate operational gains, predictive analytics embeds a data-driven culture within the finance function. It supports continuous improvement in accounts receivable performance, early detection of anomalies and faster corrective action.

Teams spend less time gathering information and more time analysing, anticipating and deciding.

Predictive analytics is a natural extension of artificial intelligence applied to collections: far beyond simple automation, it becomes a genuine financial management tool.

Predictive analytics in practice: three concrete applications

Predictive analytics delivers real value when applied directly to collections, alongside tools like LeanPay that centralise, automate and bring greater reliability to AR management.

Calculating a real-time risk score with predictive analytics

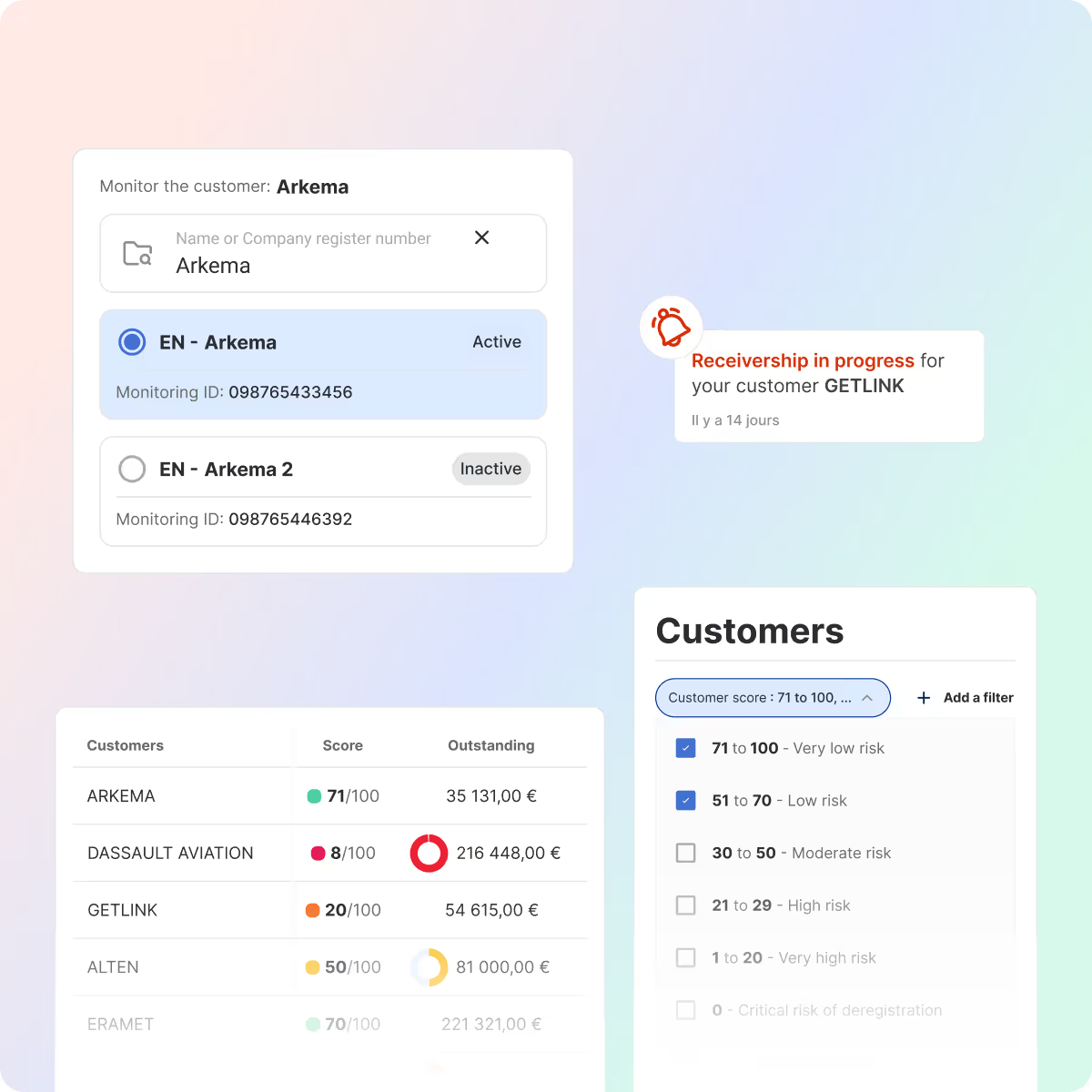

Working from the available data, the predictive model assigns each customer a risk score that is updated continuously.

This score makes it possible to identify which invoices need close monitoring, which should be chased as a priority and which can be managed through more automated workflows.

To help finance teams anticipate customer risk, LeanPay provides a credit score for each customer, updated in real time through integrations with leading financial information providers.

Prioritising and automating collection actions

Once risks have been identified, the challenge is knowing where to focus collection efforts. By segmenting the portfolio by risk level, teams have a clear view of outstanding amounts.

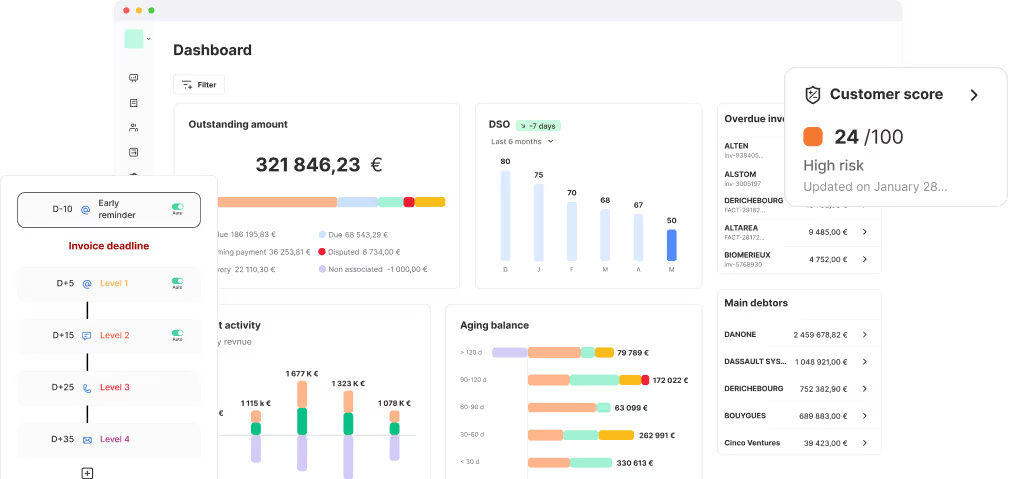

High-risk customers can be followed up more closely, with shorter intervals between reminder steps (moving from 10 days to 5 days, for example).

Moderate-risk customers receive adapted messaging and frequency, while reliable payers are managed through lighter-touch workflows.

This dynamic segmentation makes it possible to tailor the collections approach to each customer profile, without multiplying manual tasks.

With LeanPay, payment reminders can be sent automatically or triggered after manual review. They are fully customisable in terms of frequency, content and channel (SMS, phone, email, letter).

Automation saves teams significant time while keeping them in control of personalisation and follow-up.

Monitoring and adjusting with predictive intelligence

Predictive analytics also supports dynamic dashboards: DSO trends, prediction accuracy rates, risk profiles across the customer base. Finance teams can adjust their priorities based on observed trends and continuously improve overall accounts receivable performance.

LeanPay already gives finance teams a complete, up-to-date view of their AR through the accounts receivable dashboard. Outstanding amounts, DSO, aging balance and more are all available in a centralised, customisable dashboard. Updated in real time, this data provides a clear and actionable read on collections performance.

.png)

More than 3 000 finance teams use LeanPay to optimise their accounts receivable. Get in touch to find out how you can do the same.

Obtenir le modèle :

Obtenir le modèle :